Why Mortgage Rates Move Even When the Bank of Canada Does Nothing

Most people assume mortgage rates move because the Bank of Canada says so.

It makes sense.

You hear about a Bank of Canada announcement in the news, then everyone starts asking whether mortgage rates are going up, going down, or staying the same.

But here’s the part many Canadians do not realize:

The Bank of Canada is important, but it is not the whole story.

In fact, one of the biggest reasons people feel confused about mortgage rates is because fixed mortgage rates and variable mortgage rates do not work the same way.

So when people ask me, “Why did rates move if the Bank of Canada did nothing?” this is usually where the conversation starts.

Mortgage rate pricing is more complicated than most people think.

That does not mean you need to become an economist.

But it does mean understanding the basics can help you make smarter decisions when you are buying, renewing, refinancing, or comparing mortgage options.

Why Mortgage Rates Move: The Bank of Canada Is Only One Part

When people talk about Bank of Canada mortgage rates, they are usually referring to the overnight rate.

That overnight rate influences the Prime rate, which is used by banks and lenders for many variable-rate products.

So yes, when the Bank of Canada changes its policy rate, it can affect variable mortgage rates Canada, lines of credit, and other Prime-based borrowing products.

But fixed mortgage rates Canada are different.

Fixed rates are usually influenced more by the bond market than by the Bank of Canada’s rate announcement itself.

That is why you can sometimes see fixed rates rise even when the Bank of Canada holds steady.

It is also why fixed rates may not drop right away after a Bank of Canada cut.

This is one of the key things to understand about why mortgage rates move.

There is not just one switch that gets flipped.

There are multiple forces working behind the scenes.

Why Mortgage Rates Move Differently for Fixed and Variable Mortgages

A lot of confusion comes from putting fixed and variable mortgages into the same bucket.

They are both mortgages, but they are priced differently.

Variable Mortgage Rates Canada Are More Closely Tied to Prime

Variable mortgage rates Canada are usually based on the lender’s Prime rate, plus or minus a discount or premium.

For example, a lender might offer Prime minus a certain percentage.

When the Bank of Canada changes its policy rate, lenders often adjust Prime shortly after.

That means variable-rate borrowers may feel the impact more directly.

If rates go down, variable-rate borrowers may benefit.

If rates go up, they may pay more interest or see payments increase, depending on the type of variable mortgage they have.

This is why people often connect the Bank of Canada directly with mortgage rates.

For variable rates, that connection is much more obvious.

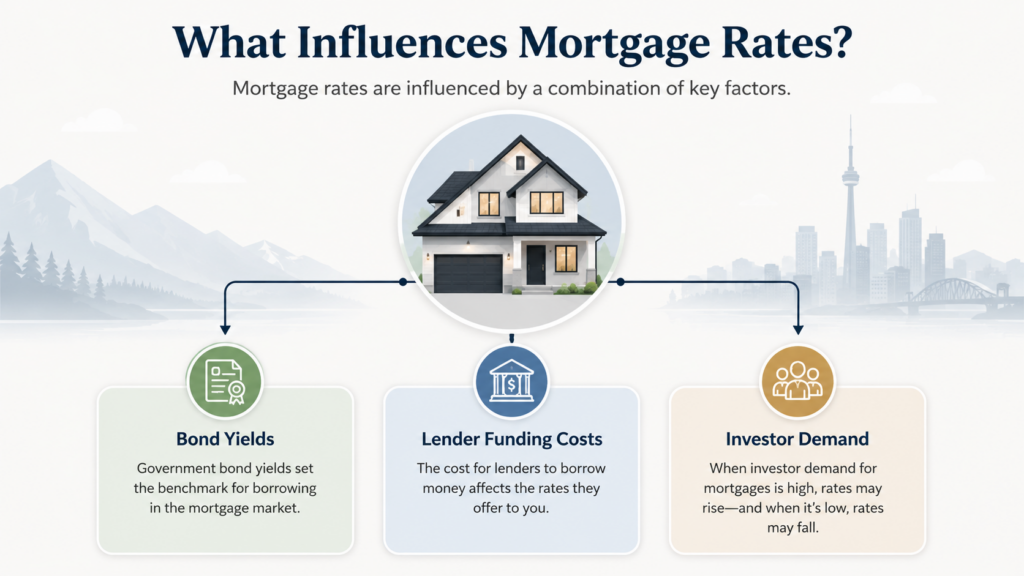

Fixed Mortgage Rates Canada Are More Connected to Bond Markets

Fixed mortgage rates Canada are more closely connected to the bond market.

More specifically, lenders look at things like bond yields Canada, market expectations, funding costs, and investor demand.

When bond yields rise, fixed mortgage rates often rise too.

When bond yields fall, fixed rates may become more competitive.

This is why fixed rates can change before the Bank of Canada makes a move.

Markets are always trying to price in what they think will happen next.

So if investors believe inflation may stay higher, or the economy may shift, bond yields can move.

And when bond yields move, fixed mortgage rates can follow.

That is a major reason why mortgage rates move even when the Bank of Canada has not changed anything.

Why Mortgage Rates Move Before Announcements Happen

Here is something that surprises a lot of people:

Mortgage rates can move before a Bank of Canada announcement.

Why?

Because financial markets do not wait for the news to become official.

They react to expectations.

If investors believe the Bank of Canada may cut rates later, bond yields may start moving before the announcement happens.

If investors believe inflation could be sticky, or rate cuts may be delayed, bond yields may rise before any official decision is made.

This is part of mortgage rate pricing that most consumers never see.

By the time the Bank of Canada makes an announcement, some of the expected move may already be priced into the market.

That is why a rate cut does not always create an immediate drop in fixed rates.

And that is why a rate hold does not always mean fixed rates stay frozen.

Again, this is why mortgage rates move in ways that can feel confusing from the outside.

Why Fixed Rates Change Even When the Bank of Canada Holds

Let’s say the Bank of Canada holds rates.

A lot of people assume that means mortgage rates should stay exactly the same.

But that is not always how it works.

Fixed mortgage rates can still change because lenders are looking at more than one factor.

They are watching:

- Bond yields Canada

- Funding costs

- Investor demand

- Inflation expectations

- Economic data

- Competition from other lenders

- Risk in the mortgage market

So when someone asks, “Why fixed rates change if the Bank of Canada did nothing?” the simple answer is:

Because fixed rates are not controlled directly by the Bank of Canada.

They are influenced by the broader financial market.

This is also why Canadian mortgage rates can look different from one lender to another.

Each lender may have different funding sources, different risk appetite, different investor relationships, and different business goals.

That is why two lenders can look at a similar mortgage file and offer different pricing.

Why Mortgage Rates Move Based on Lender Funding Costs

Another piece of the puzzle is lender funding costs.

Most people think of a mortgage as:

- You apply.

- The lender approves.

- The mortgage funds.

- You make payments.

That is the part the borrower sees.

But behind the scenes, lenders need money to lend.

They may fund mortgages through deposits, capital markets, mortgage-backed securities, insured mortgage pools, or other funding channels.

That money has a cost.

When it becomes more expensive for lenders to access funds, mortgage rates can increase.

When funding becomes cheaper or competition increases, rates may become more attractive.

This is one reason mortgage rate pricing is not always as simple as “the Bank of Canada did this, so mortgage rates should do that.”

Lenders are pricing based on their own costs too.

And those costs can vary.

Why Mortgage Rates Move Based on Investor Demand

Investor demand also plays a role.

This is one of the most overlooked parts of the mortgage world.

Many mortgages are not just held quietly by one lender forever.

Behind the scenes, mortgages can be insured, pooled, packaged, and sold to investors.

That matters because investors want to understand the risk and return of the mortgage products they are buying.

If investors are comfortable with the risk, lenders may be able to access cheaper funding.

If investors want a higher return because they see more risk, the cost of funding can rise.

That can affect Canadian mortgage rates.

This is part of why mortgage rates move in ways that may not feel obvious to the average borrower.

Your mortgage is not just a loan sitting in a file somewhere.

It is part of a much larger financial system.

Why Insured Mortgages Can Sometimes Get Better Rates

This is another part of mortgage pricing that surprises people.

Sometimes, a borrower with less than 20% down can get a better rate than someone with a larger down payment.

At first, that sounds backwards.

But here is why it can happen.

When you buy with less than 20% down in Canada, mortgage default insurance is usually required through CMHC, Sagen, or Canada Guaranty.

Important note: this is not life insurance or disability insurance.

Mortgage default insurance protects the lender if the borrower defaults.

Because the lender has more protection, the mortgage can be less risky from a lending and investor perspective.

Lower lender risk can sometimes lead to better pricing.

This does not mean putting less than 20% down is always better.

You still need to consider the insurance premium, your payment, your long-term cost, and your overall plan.

But it does explain why mortgage rate pricing sometimes works differently than people expect.

The mortgage world is not always logical from the outside.

Why Mortgage Rates Do Not Tell You Which Mortgage Is Best

Here is where I want to be really clear.

Understanding why mortgage rates move is helpful.

But it still does not tell you which mortgage is best for you.

The best mortgage rate Canada is not always the best mortgage.

Rate matters, obviously.

Nobody wants to pay more than they need to.

But rate is only one part of the decision.

You also want to look at:

- Penalties

- Prepayment privileges

- Portability

- Refinance flexibility

- Renewal options

- Term length

- Fixed vs variable mortgage rates

- Your cash flow

- Your future plans

A slightly lower rate may not help much if the mortgage comes with restrictions that cost you later.

For example, if you need to break the mortgage early, refinance, move, or access equity, the penalty and flexibility can matter a lot.

This is why mortgage broker advice can be so valuable.

A broker is not just looking for a number on a rate sheet.

A broker should be helping you understand the full mortgage structure.

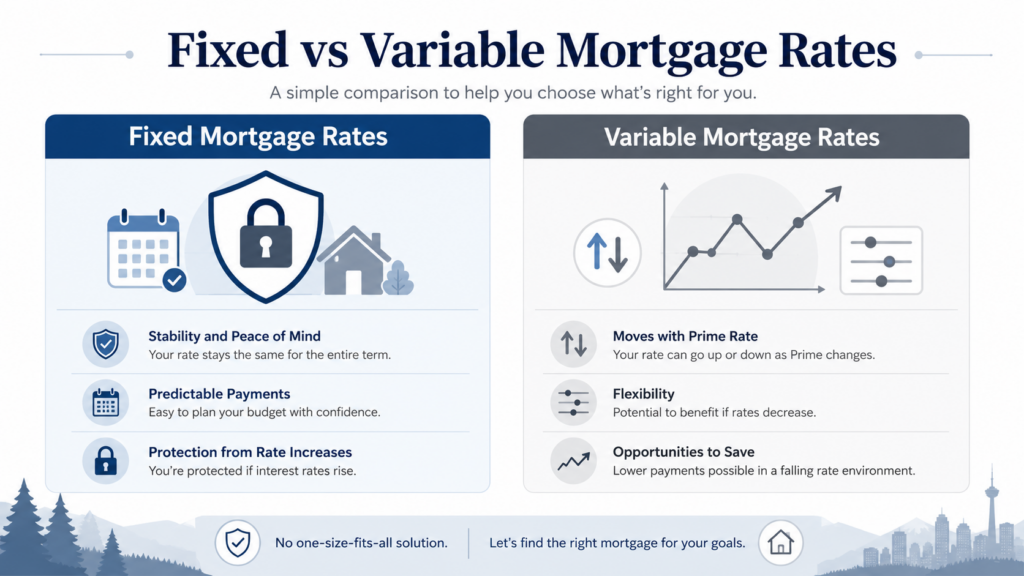

Fixed vs Variable Mortgage Rates: What Should You Focus On?

When comparing fixed vs variable mortgage rates, the better question is not always “Which one is cheaper today?”

A better question is:

Which one fits your life?

A fixed rate may make sense if you want payment stability and certainty.

A variable rate may make sense if you are comfortable with some risk and want the potential to benefit if rates move lower.

A shorter-term fixed mortgage may make sense if you want some stability but also want flexibility sooner.

A longer-term mortgage may make sense if you want more certainty and do not plan to make major changes.

There is no universal answer.

The right choice depends on your income, comfort level, timeline, future plans, and how much payment uncertainty you can handle.

This is another reason why mortgage rates move is only part of the conversation.

The bigger conversation is what mortgage strategy fits your situation.

Why Mortgage Rate Moves Matter When You Are Renewing

If your mortgage is coming up for renewal, understanding why mortgage rates move can help you avoid making decisions based only on headlines.

A lot of people wait for a Bank of Canada announcement and assume they should decide right after.

But your renewal strategy should be based on more than one announcement.

You want to look at:

- Your current lender’s offer

- Competing lender options

- Fixed and variable pricing

- Payment comfort

- Penalty risk

- Whether you may move or refinance

- Whether your debts or cash flow have changed

Sometimes waiting makes sense.

Sometimes it does not.

Sometimes a shorter term makes sense.

Sometimes stability is worth more than trying to guess the next rate move.

The point is not to predict everything perfectly.

The point is to make a decision that fits your life.

Why Mortgage Rate Moves Matter When You Are Buying

If you are buying a home, mortgage rate changes can affect your budget.

But I would not recommend building your entire plan around trying to time the perfect rate.

Rates can change.

Bond yields can move.

Lender pricing can shift.

Your approval can also depend on income, credit, down payment, debt, property type, and lender guidelines.

That is why a proper pre-approval matters.

Not a quick online estimate.

A real review of your numbers.

When you know your actual budget, your comfortable payment, and the type of mortgage that fits your situation, you are in a much stronger position.

That matters more than trying to guess exactly where Canadian mortgage rates will be next month.

Why Mortgage Rate Moves Matter When You Are Refinancing

If you are thinking about refinancing, understanding why mortgage rates move can help you look at the full picture.

For example, you may be focused only on whether today’s rate is higher or lower than your current mortgage rate.

But refinancing is not always about getting a lower mortgage rate.

Sometimes it is about improving monthly cash flow, consolidating higher-interest debt, accessing equity, or restructuring your mortgage so your finances feel more manageable.

That does not mean refinancing is always the right move.

It means the decision should be based on the math.

You need to compare:

- Current mortgage rate

- New mortgage rate

- Penalty to break the mortgage

- Debts being consolidated

- New payment

- Total monthly cash flow

- Long-term cost

- Future flexibility

This is why mortgage broker advice matters.

The right answer is not always obvious from the rate alone.

Final Thoughts: Why Mortgage Rates Move Is Only Part of the Story

So, why mortgage rates move even when the Bank of Canada does nothing?

Because the Bank of Canada is only one part of the mortgage rate story.

Variable rates are more closely tied to Prime.

Fixed rates are more closely connected to bond yields Canada, lender funding costs, investor demand, and market expectations.

Lenders also price mortgages based on risk, competition, mortgage type, insurance, and their own funding model.

That is why mortgage rates can feel confusing.

It is also why advice matters.

The goal is not just to find the lowest rate.

The goal is to find the mortgage that fits your life, your budget, your future plans, and your comfort level.

If you are buying, renewing, refinancing, or just trying to understand what today’s mortgage rates mean for you, reach out before making a decision.

A short conversation can help you understand your options clearly and avoid choosing a mortgage based on one number alone.

First Home Savings Account (FHSA)

First Home Savings Account (FHSA)